In my last article, I wrote on two key challenges, we as Robo-advisors face; i.e. “Customer mind-set” towards investments, where it comes as last priority and “Meaning of investments”, where quality is not understood.

To sum it up… how do you motivate customers?

Unlike e-commerce portals, based on current theme, it’s the deep discount that attracts. We have cases (many); where customer go to malls or retail outlet on look & feel, and finally will swap on their smart phone to check on availability & discount, and punch the order… which is obvious, where?

(more…)

Manoj Chahar

July 16, 2016

Financial Planning, Investmentsinvest 500, investments, small investments, small investments big returns

Read more >

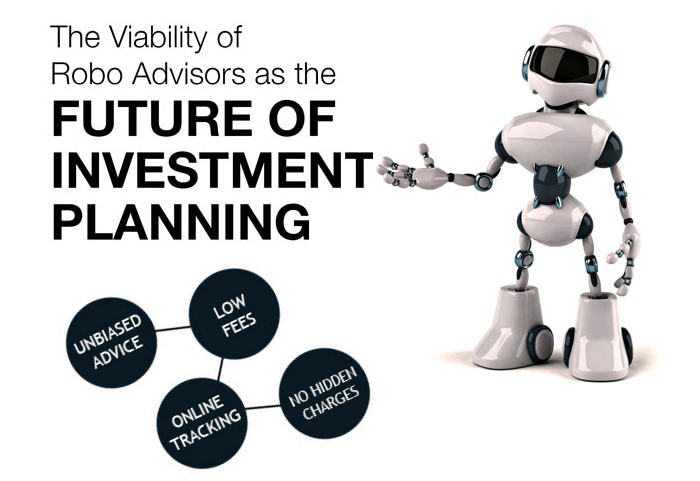

As per Wikipedia; “Robo-advisors are a class of financial adviser that provides financial advice or portfolio management online, with minimal human intervention”.

Most Robo-advisors employ algorithms, where automated investment solutions come out as output, based on customer’s data points; towards cash flow, future goals, risk tolerance, current investments etc.

Logic & working of these algorithms, which can be simple to complex, depends on the solutions offered to various category of customers, which also depends on firm’s/ founders experience & expertise.

Indian Context

(more…)

Manoj Chahar

July 8, 2016

Robo Advisorsgoal base robo advisors, robo advisors, robo advisors- Future of investments

Read more >

Brexit, a referendum on UK, whether to stay in the European Union or not, is finally over with 52% voters demanding an EXIT (48% is in favour of European Union). Sensex which opened with a gap of 1000 points today, with some recovery closed with 600 points down. International markets went for a full hara-kiri with 5% to 10% dive.

Will it affect India?

With European Union (EU) losing one of its members, India too can feel the heat. Rupee may depreciate because of the double effect of foreign fund outflow and dollar rise, and may lead to increase in petrol and diesel prices to an extent. The government then may want to reduce additional excise duty imposed on fuel when it was on a downward trajectory. This will

(more…)

Manoj Chahar

June 25, 2016

InvestmentsBrexit, european union, stock markets

Read more >

There are many milestones of being an adult. Signing your own lease for the first time, being able to rent a car, having someone call you ma’am.

But being an adult also means being responsible for your own finances. Like many things, you can’t have a successful financial future if you don’t plan for it. The best way to do that? Create a budget.

Creating a budget can seem daunting, but it just requires a series of steps. See below for help on creating your first budget.

Track your expenses

Before you can start a budget full of limits, you need to know how much you’re spending right now. Take two or three months to spend normally and track your transactions in Moneyfrog.in.

Fixed expenses like rent, insurance and utilities will be easier to monitor than variable expenses, such as groceries, entertainment and travel, which will fluctuate month-to-month.

(more…)

Harshada Kadam

May 20, 2016

Financial Planningbudget, budget planning, budgeting, careers, college, debt, debt management, economy, education, Employment, financial management, financial planning, first budget, food, frugality, handling personal finance, making first budget, Money Management, personal finance, saving, savings, shopping, Student Loans, tips

Read more >

Harshada Kadam

October 18, 2015

Financial Planning, Infographicsguide to investing in NPS, infographics, infographics to Guide to Investing in the NPS, tips to invest into nps, Your Guide to Investing in the NPS

Read more >

Not having enough money to pay the bills is an issue we may face from time to time. Life is full of financial ups-and-downs, and after all, we’re all human.

Don’t beat yourself about the situation or get discouraged. Vow to take action. If you don’t make changes, things will stay the same. If you’re in a tough financial spot, here’s what to do when you can’t pay your bills on time, and tips on how to best handle the situation.

1. Don’t Hide From the Facts

Do you know why you can’t pay your bills? Did you overspend, have to make up for an emergency, or was it just human error? Don’t hide from the facts, but instead embrace them head-on. Not dealing with this financial mess can lead to more late fees, higher interest rates, additional interest charges, and even damage your credit report.

(more…)

Harshada Kadam

August 27, 2015

Financial Planningbudget planning, cash flow planning, planning bills and budget

Read more >

Harshada Kadam

August 21, 2015

Financial Planning, Infographicscareer opportunities, career opportunities infographic, child's education, education decision, education priorities

Read more >

If there’s one thing that all wealthy people have in common it’s this: They invest.

That’s because investing money is the smartest and most reliable way to grow it over the long term, after you have first built up your emergency savings (which never gets invested).

Investing in a Nutshell

Investing is putting your money in a financial vehicle that might enable it to grow more quickly than it would in a savings account.

While most of us think of “earning” as putting in hours of work and getting paid for that, investing essentially puts our money into a marketplace where companies and governments and other entities can use it to create a profit that will be returned to us. (At least that’s the hope—some investments do go bust, taking our money with them.)

Most commonly, people invest by buying financial assets like stocks, bonds, mutual funds and ETFs (and if you don’t know exactly what these are, don’t worry, we’ll describe them later). When we sell them, we hopefully make a profit by selling at a price higher than what we bought them for.

(more…)

Harshada Kadam

August 8, 2015

Financial Planningbonds, ETFs, investing, investment rules, Mutual Funds, online investing, stocks

Read more >

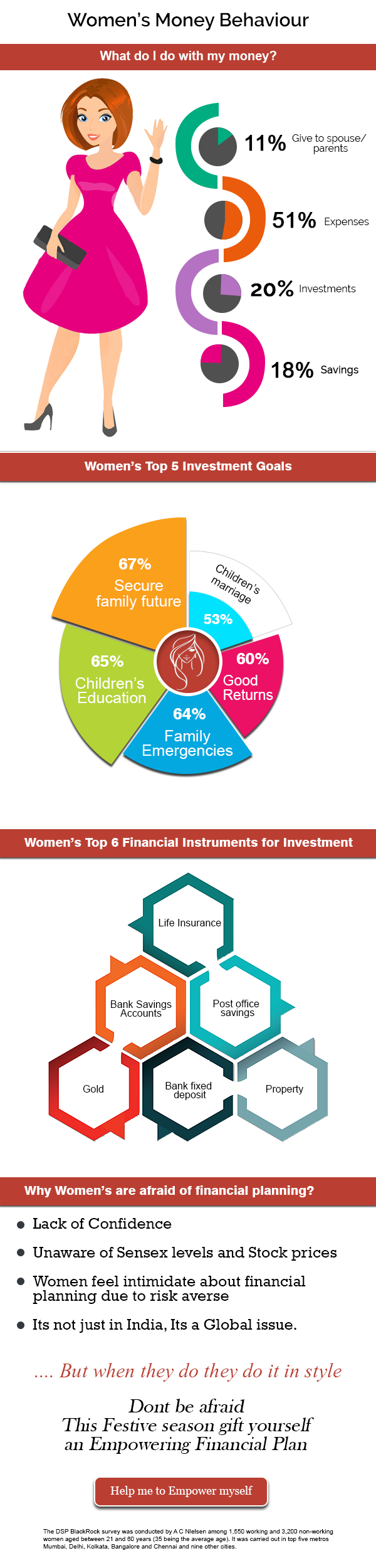

Harshada Kadam

August 5, 2015

Financial Planning, Infographicsfinancial instruments for investments, investment goals, women's money behaviour

Read more >

Even though consumers have been using online banking and mobile applications for years, the concept of online financial planners like Moneyfrog.in is still new. In comparison to a traditional face-to-face financial planning relationship, how do online financial planners work?

Online financial planners allow you to:

- Develop plans for your finances that are comprehensive enough to include every aspect of your life from buying new home, child education, insurance, long-term investment management, spending trends, and retirement.

- Analyse your debt, understand how debt management works, and develop a plan to pay down debt.

- Access finances at any time. You don’t need to make appointments with a financial planner, or schedule an office visit plus travel time.

- Analyse your financial situation and run scenarios to cover “what if” questions about your financial future. You can change your financial plan at no extra cost.

- Keep your information private. Unlike a traditional financial planner, no one else needs to see your personal information, and you can rest assured your information is stored securely.

- Run quick reports, and understand them easily.

(more…)

Manoj Chahar

July 26, 2015

Financial Planningfinancial advice, financial advisors, financial calculators, financial planners, financial planners in mumbai, financial planning, goal tracking, how financial planners work, mobile app, online financial planning, portfolio and asset tracking, risk analysis

Read more >