Market Outlook – July 2020

In the last month, the market has delivered a stupendous return of around 7.5%, this is despite the geopolitical tension seen in the India – China border. The main reason behind this sharp increase was the availability of global liquidity with institutional investors, what we have seen is a coupling effect and this rise in equity was witnessed globally across the markets.

Certain companies, especially the one who are largely affected by this lockdown, are expected to defer or merge their quarterly result to soften the impact seen in top-line of Q1 strict lockdown with Q2 quarter with a partial lockdown. Some investors are concerned about market valuations due to current gains seen in the market since on earnings parameters it appears to be expensive, it is fallacious to conclude by just seeing one parameter. Investors must adhere that earnings are just a perspective like other ratios viz Price to book value and Market cap to GDP. Many other ratios still suggest the market being at an attractive valuation due to sharp correction so investors who have missed previous opportunities have not really missed the bus yet. Also, the volatility index though relatively high but has fallen drastically which indicates that the market is closer to trade at the fair market value range.

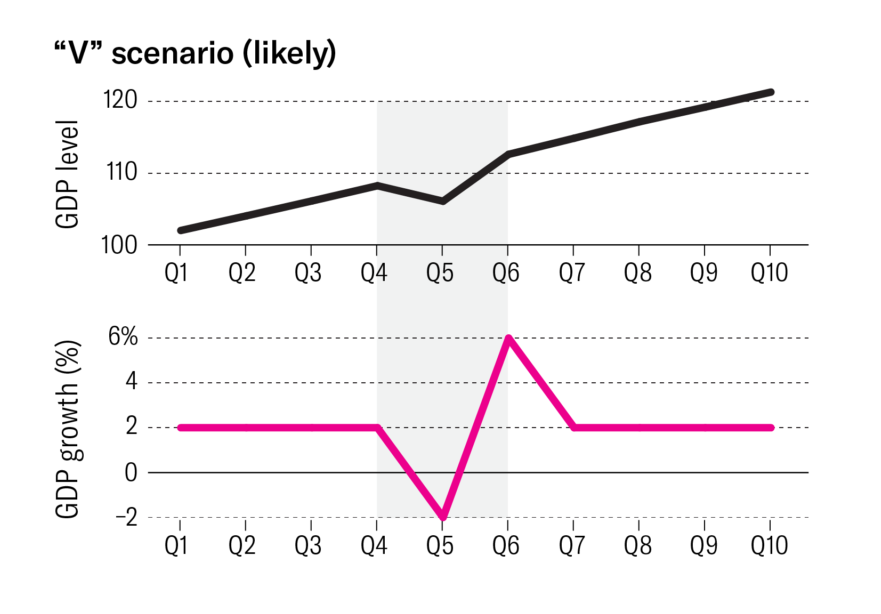

Global economy is headed for its sharpest contraction but by comparing previous historic events and market reaction, the current phase has seen lesser correction and the recovery seen is quicker since learnings from previous such events has made global leaders more competitive to react proactively and with the amount of liquidity injected into the financial system will prevent the stalling of the economy to a larger extent and the recovery expected is to be relatively quicker.

The government is also expected to announce another fiscal stimulus which will mainly address the demand issue and boost consumption and investment sentiments.

Stay Safe!

Photo credit: edelweiss.in