Retirement Planning- How aware are you?

While people are realising the need to save for sunset years, they are still investing in fixed income plans, says the recent RMF-IMRB retirement survey. Here are some other findings.

While people are realising the need to save for sunset years, they are still investing in fixed income plans, says the recent RMF-IMRB retirement survey. Here are some other findings.

October 18, 2015 Financial Planning, Infographics 0 Read more >

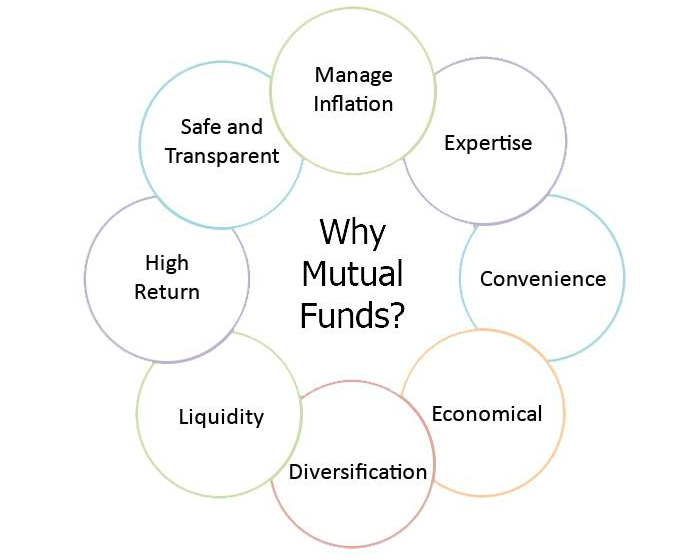

When considering investment opportunities, the first challenge that almost every investor faces is a plethora of options. From stocks, bonds, shares, money market securities, to the right combination of two or more of these, however, every option presents its own set of challenges and benefits.

So why should investors consider mutual funds over others to achieve their investment goals?

Not having enough money to pay the bills is an issue we may face from time to time. Life is full of financial ups-and-downs, and after all, we’re all human.

Don’t beat yourself about the situation or get discouraged. Vow to take action. If you don’t make changes, things will stay the same. If you’re in a tough financial spot, here’s what to do when you can’t pay your bills on time, and tips on how to best handle the situation.

1. Don’t Hide From the Facts

Do you know why you can’t pay your bills? Did you overspend, have to make up for an emergency, or was it just human error? Don’t hide from the facts, but instead embrace them head-on. Not dealing with this financial mess can lead to more late fees, higher interest rates, additional interest charges, and even damage your credit report.

August 21, 2015 Financial Planning, Infographics 0 Read more >

If there’s one thing that all wealthy people have in common it’s this: They invest.

That’s because investing money is the smartest and most reliable way to grow it over the long term, after you have first built up your emergency savings (which never gets invested).

Investing in a Nutshell

Investing is putting your money in a financial vehicle that might enable it to grow more quickly than it would in a savings account.

While most of us think of “earning” as putting in hours of work and getting paid for that, investing essentially puts our money into a marketplace where companies and governments and other entities can use it to create a profit that will be returned to us. (At least that’s the hope—some investments do go bust, taking our money with them.)

Most commonly, people invest by buying financial assets like stocks, bonds, mutual funds and ETFs (and if you don’t know exactly what these are, don’t worry, we’ll describe them later). When we sell them, we hopefully make a profit by selling at a price higher than what we bought them for.

August 5, 2015 Financial Planning, Infographics 0 Read more >

Even though consumers have been using online banking and mobile applications for years, the concept of online financial planners like Moneyfrog.in is still new. In comparison to a traditional face-to-face financial planning relationship, how do online financial planners work?

Online financial planners allow you to: