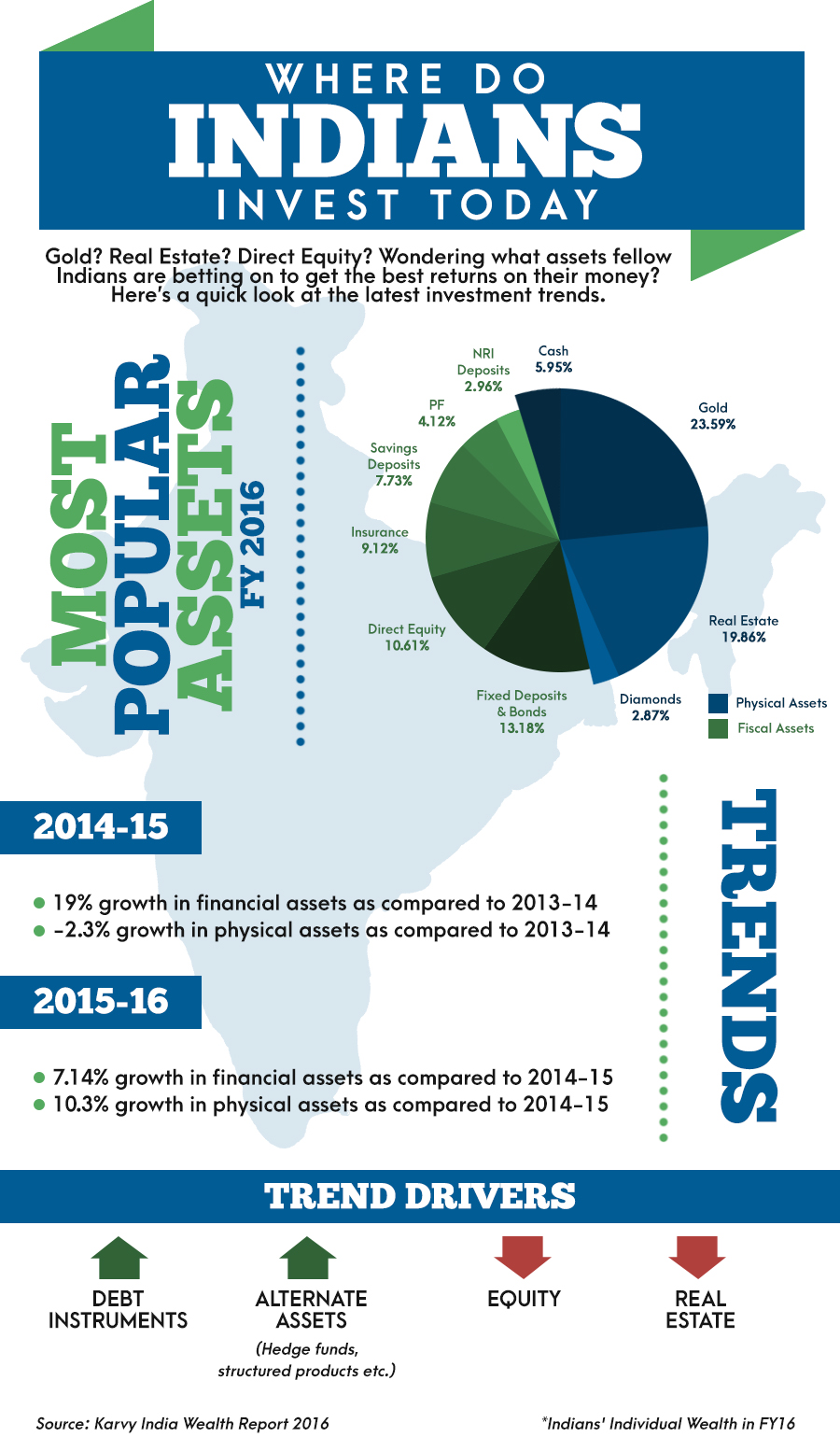

Where Do Indians Invest?

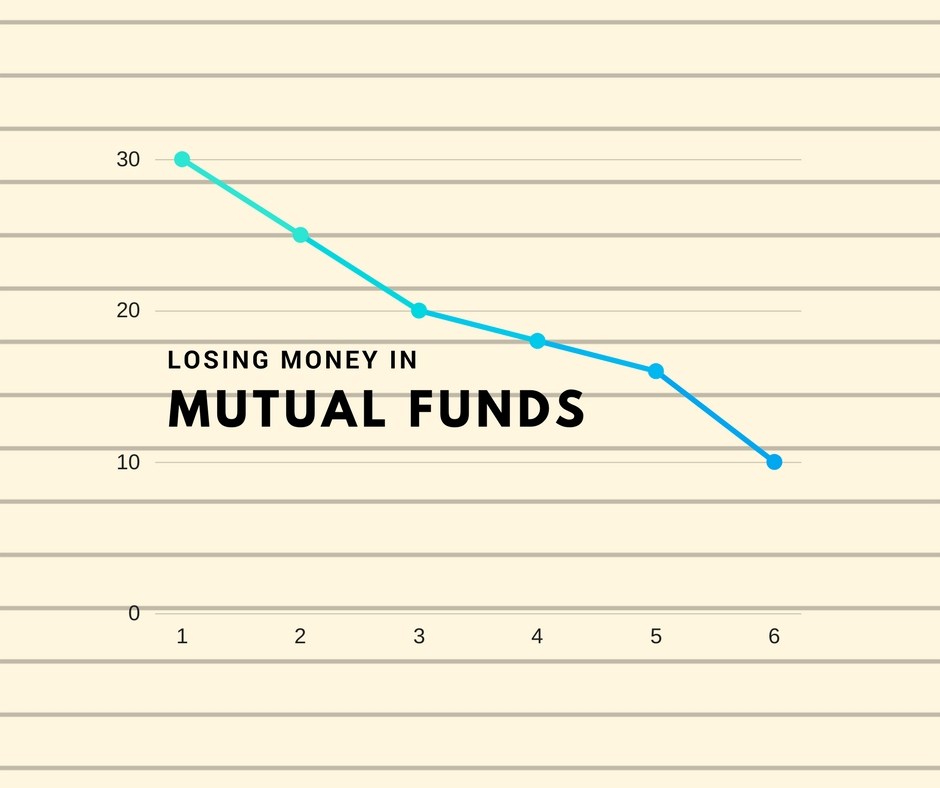

I’m investing in the best performing mutual fund schemes, but after I invest, the fund’s performance starts degrading. What do I do?

This is the story with each one of us. When NAV is low, FEAR factor surrounds us (what to do now?) & when NAV is high, we have GREED (to hold on or to buy more?).

It’s like planting a tree, once the seed is planted, we virtually see it every day, to check on the growth. First few days/ weeks are very exciting, when we see a small bud, leaves sprouting; but after few weeks or a month, it becomes frustrating, as growth is small & we want to see a big tree right away. Whereas it will take years, before the tree is fully formed, will bear flowers & fruits, and above all it must withstand harsh weather& other factors.

Equity market reacted to two key events yesterday, with Sensex going down 1314 points intra-day or 3.5%.

While Yes Bank corrected because of RBI’s denial of tenure extension to the CEO Mr. Rana Kapoor, the fall in shares of DHFL was driven by sale of the company’s debt by a mutual fund at higher yields.

What comes out is the fact that, in the broader markets, this was a knee jerk reaction and prices of most stocks should stabilize once the panic subsides.However, the sharp volatility witnessed, highlights the underlying fragility of the market.

It’s true that the selling was largely sentiment driven with no fundamental negatives in most stocks. However, the price action with almost no buying interest characterizes a market where risk appetite is low.

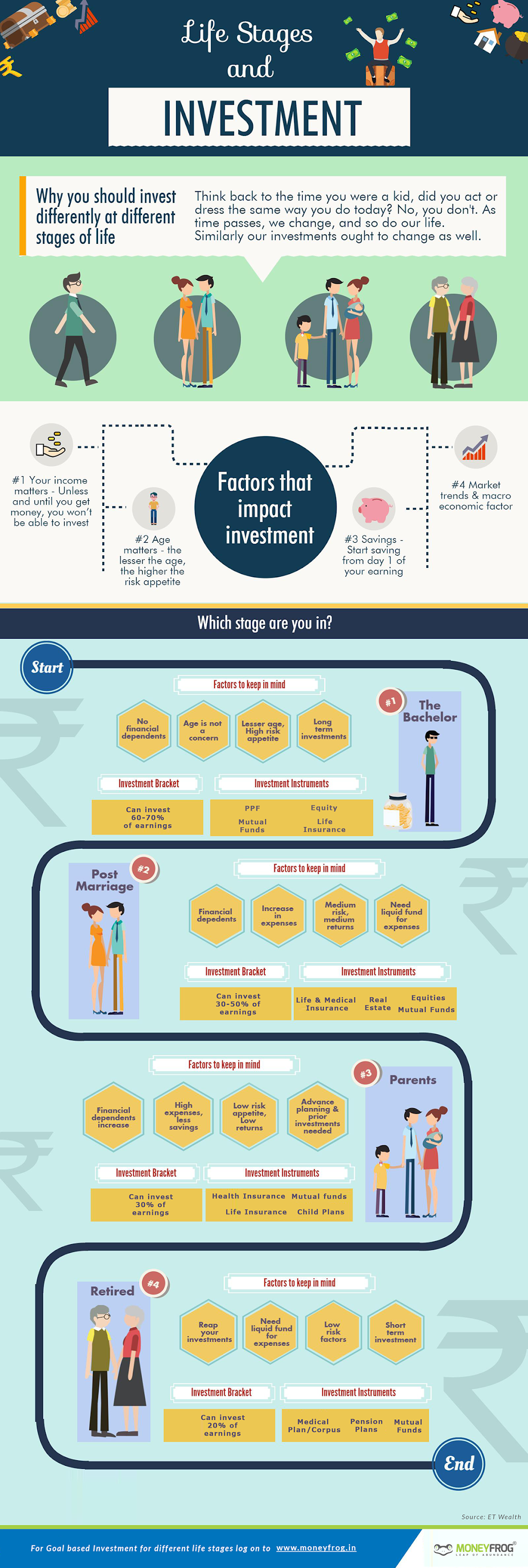

Your income, priorities and spending habits changes depending on your life stages. This infographic will guide you how to plan your finances for different life stages.

Source: ET Wealth

As an investor in Mutual Funds, we all come across these terms, very often.

What it means?

Which one to use?

Which one is the best?

Let’s simplify…

CAGR; stands for “Compounded Annual Growth Rate”, and works on a compounding formula, based on a single transaction. Usually CAGR is used for estimating future returns, based on historic returns or assumptions, for a time range.

IRR; stands for “Internal Rate of Returns”, and used for calculating returns for multiple transactions, which are equally spaced in time (past or future). Usually IRR is used for calculating returns for SIP transactions.

XIRR; stands for “Extended IRR”, like above, only difference being, when your transactions are not equally spaced in time. For instance, calculating returns for transactions, which may include SIP, Lumpsum, STP, SWP, etc.Absolute returns; refers to the amount of funds (gain or loss), that an investment has earned, over a period of time. Also referred as the “Total Return”, the “Absolute Return” measures the gain or loss experienced by an asset or portfolio.

Its shocking to see Rupee’s free fall from 65 to 70,& within last few days to 72 today, against USD. Some of the key reasons which are supporting this downfall, are international events. Experts fell that this volatility will continue for some time to come (one to three months) and stability by Mar-19 or earlier, where Rupee to become stable or under 69.

Some of the key events:

USD & Crude Gaining Strength: USD is gaining strength back home with quantitative tightening & interest rates, leading to drying liquidity. This easy money earlier was chasing emerging market assets (in order to generate higher returns). Rise in crude prices on the other hand is playing spoilsports.

One of the retirement strategies; comes from a paper written in 1998 by three finance professors at Trinity University. Idea was to study & identify, as to what rate of withdrawal is an ideal rate per year, which is sustainable to the retirement corpus, and can last 30 years.

How the 4% rule works?

To figure out how much money you need for your retirement corpus, multiple 25 with the annual retirement income (you wish that point of time). Let’s say you need 10 lacs per year.

In just one-month, Sensex has climbed 3000 points, or jumped straight 8.5%. Till June end, everyone was worried, as market has had a very volatile phase (since last six months). As usual, question is, whether one has missed the bus? or the rally has just started?

Let me highlight on the macro trends:

Crude Oil: 70% of the demand for crude oil comes from transport. Alternative for crude oil is Electronic cars, which will become accessible in another 10-15 years (crude reserves are expected to last 50-80 years). Average crude oil price (for India) should range between USD 55-65, because this price doesn’t affect our foreign reserves.