Make sure returns on your investments are ahead of inflation; while equity funds are the best option, monthly income plans can be a good alternative

The inflation monster is beginning to stir again. Consumer inflation rose to 6.07% in July due to higher food prices and analysts expect no respite in the coming months.Most readers may not get perturbed if prices rise by around 6% in a year.But this is a misleading figure because it represents the inflation faced by all consumers, including the vast lower middle class. “Middleand upper-middle class consumers experience a significantly higher inflation than what the index indicates,“ says Debopam Chaudhuri, chief economist, ZyFin Research.

The index itself does not truly reflect the expenditure of the average middleand upper-middle class family. For example, education has less than 6% weightage in the index for urban consumers even though almost 10-12% of the expenses of urban Indian families go towards this.

“The CPI inflation is not relevant for financial planning as the basket and proportion of items are vastly different from the actual consumption by families,“ says Chenthil Iyer, founder of financial advisory firm Horus Financial Consultants.

Also, the index puts the rise in education inflation in the past year at 4.3% whereas the fees in public schools and other ancillary expenses are going up by nearly 8-10% every year. Higher education costs are rising at an even faster clip of 10-12%.These numbers are critical. If parents investing for their child’s education assume a lower inflation of 6-7%, they could end up saving a much lower amount than required.

Here’s a perspective of how wrong can one go by following the index. If an engineering course costs 8 lakh in 2016 and the investor assumes the fee will rise by 7% every year, he will target a corpus of 22 lakh in 15 years. But if the fee rises 10% every year, he will require 33 lakh-50% more than what he has saved.

It is, therefore, essential that investors assume a higher inflation rate when saving for long-term goals.

“We assume education inflation at 10% and healthcare inflation at 1215% when we formulate a financial plan,“ says Taresh Bhatia, partner, Advantage Financial Planners.

The risk of going wrong is greater for those saving for retirement. It might be too late to make amends by the time they discover the miscalculation and the resultant shortfall.

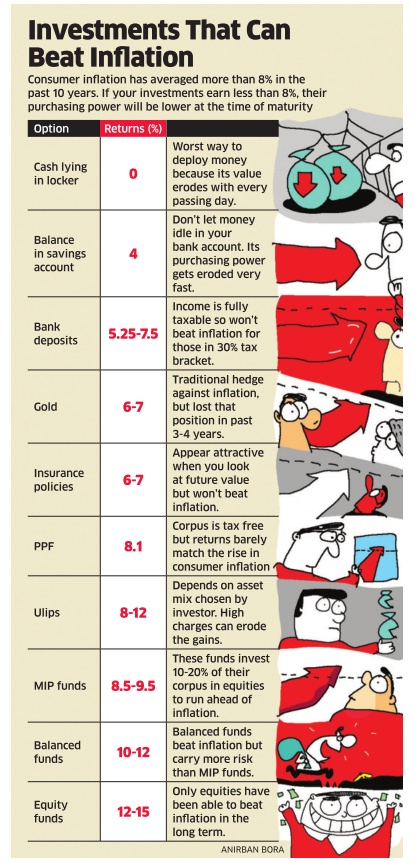

You can’t control inflation but you can insulate yourself against it.Remember, a 100% debt-based portfolio will never be able to beat inflation.

In the past 10 years, the CPI for urban consumers has risen by an average 8.07%. If your investments have earned less than 8% returns, their purchasing power is less than what it was at the time of investment. Stocks and equity-oriented funds have a good long-term record of beating inflation. In the past 10 years, equity funds have delivered 12-15% retur ns, while equity-oriented balanced funds have given 10-12%.

If your risk appetite is lower, monthly income plans (MIPs) from mutual funds can be a good alternative. These funds put only 15-20% of their corpus in equities and are therefore, less volatile than equity or balanced funds. In the past 10 years, MIPs have given around 9% returns, enough to beat inflation by a small margin.

On the other hand, life insurance plans offer 5-6% returns, but investors tend to fall for the enormous maturity corpus projected by agents. A maturity corpus of 30 lakh might seem like a big amount today , but 8% inflation will reduce its purchasing power to barely 4.5 lakh in 25 years.

Source: Economic Times