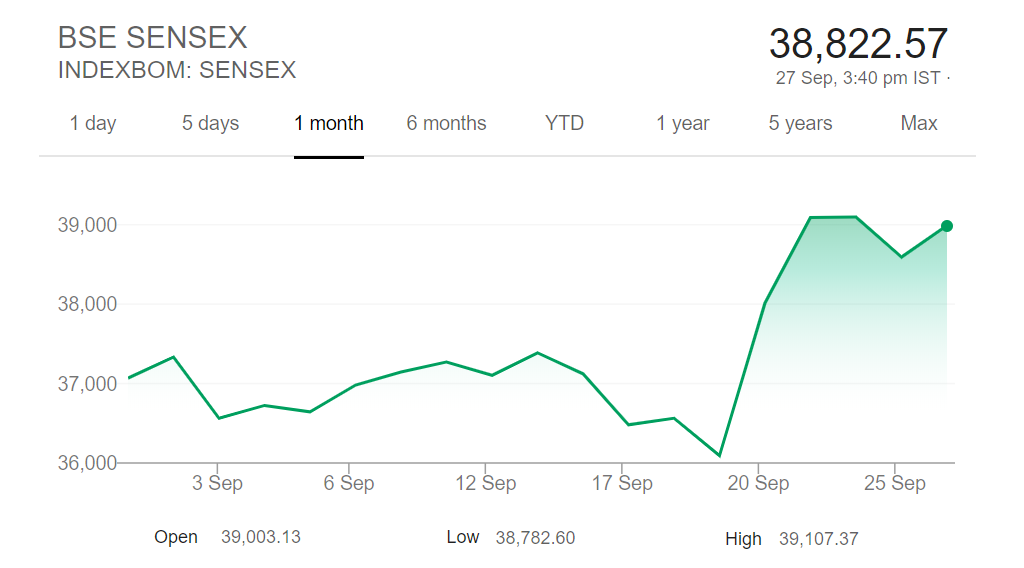

Indian Benchmark indices carried out gains of 20th September throughout the week, on a positive decision of a cut in corporate tax rate by our dear Finance Minister earlier.

Many of us were caught in the middle, what to do next?

Sensex and Nifty remained volatile due to low Global clues like US political issues, issues related to US-China trade disputes, with three sessions ended in a positive bias, out of 5 sessions. Sensex settled at 38822 & Nifty 11512, cheering up everyone’s mood & sentiment.

Asian market was trading at a mix territory, whereas European stock went-up on a hope of easing economic growth concerns.

Outlook over coming week remains Positive, on a domestic front; due to supportive sentiments, and outcome from finance minister meeting with Bank Heads, and on the international front; hope of development in the Global front, FII/FPI’s buying, easing crude prices.

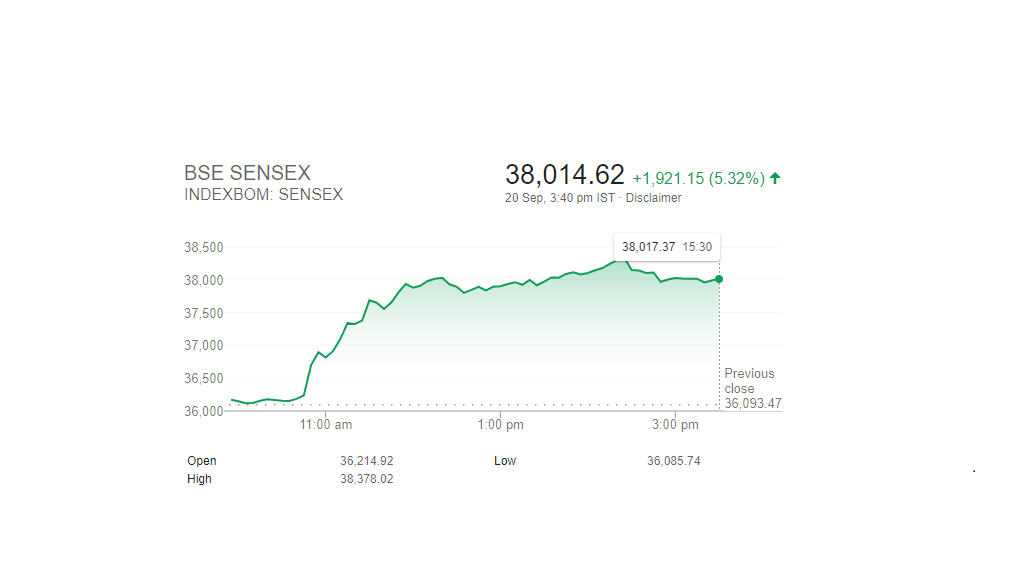

Like a blockbuster movie’s Day1 opening, today’s announcement by our dear FM Nirmala Sitharaman, pulled the market up by 2000+ points, like there is no tomorrow, snapping losses of last few weeks in a historical single day gain (in last Ten years).

Sensex settled at 38014, a gain of 5.32% percent!! Aggressive buying was seen in banks, auto and metal stocks. IT shares lagged the broader rally, as rupee edged higher at 71.12.

Asian stocks also ended higher on Friday, as economic stimulus around the world eased fears of economic deceleration. On the trade front, Chinese and U.S. delegates are meeting Thursday and Friday ahead of higher-level meetings expected early October to resolve the year-long trade dispute.

Stimulus announced by FM Nirmala Sitharaman on Friday are:

Corporate tax slashed to 22% for domestic companies, subject to condition they will not avail any incentive or exemptions (the effective corporate tax rate after surcharge will stand at 25.17%).

Manufacturing companies set up after October 1 to get an option to pay 15% tax (17.01% inclusive of surcharge & tax)

Listed companies that have announced buyback before July 5, 2019, tax on buyback of shares will not be charged

To provide relief to companies availing of concessions and benefits, a MAT relief by reducing it from 18% to 15%

Higher surcharge will also not apply on capital gains on sale of security including derivatives held by FPIs

Last night we ganged up for dinner, to celebrate my dear friend’s

birthday. Amid talks on life, markets and bosses, one specific topic that

caught everyone’s attention was that our birthday girl gifted herself a Scooty!

She narrated her story on how she was saving for over a year to buy this

Scooty, and how her travel will now be so damn easy. Sounds so nice.

As usual, one of us, the Wise-guy interrupted, giving Gyan on

using the EMI option, thru which the birthday girl could have got the Scooty much

earlier. To this, our birthday girl smiled and replied that she doesn’t like a

loan on her head, also the interest on the loan would just add up on the

burden. Saving is easy for her, living with a loan (however small), is

difficult. Though that’s her perspective, but not many of us bought this logic

last night 😉.

It’s

the same story across the millennials, where instant gratification is the buzz word.

IPhone-11 will be launched on Sept 27th, and I know many of us are

just waiting for the day to grab & show the latest asset around.

It all looks attractive (EMI I mean), but none of us gets down to

calculate the devil in it, the interest we end up coughing, to achieve this

goal. Let’s understand this thru a very basic example, i.e. Rs.5,000/- paid as

EMI for 12 months and Rs.5,000/- saved as SIP for 12 months.

EMI Option: Rs.5000/- EMI per month, for 12 months means that,

one can purchase product worth Rs.56,275/- only, as rest of the amount i.e.

Rs.3,725/- will be paid as Interest to the bank. Noting comes free.

Savings (SIP) Option: Rs.5000/- saved

per month, for 12 months goes to a RD account in bank, @8%, end of year one

will have Rs.62,665/-in the account or Rs.6,390/- extra compared to EMI

above. On the other hand, if same goes to Mutual Funds, with higher

returns, depending on tenure & risk profile, this extra amount could be

more.

Idea

is not about the last minute purchase, but the discipline to start savings at

the first instance, i.e. first salary… which also means, since I started saving

from day 1, I can literally buy my IPhone-11 costing 65k on Sept 27th

😉.

It’s not about the 1951 Alfred Hitchcock psychological thriller, but about my commute, and an invigorating conversation with a stranger 😉.

Few days back, while travelling home from the office, a co-passenger in metro asked me directions to an address. The chat started through an address, which I explained him descriptively. He shared some details about him business travel and told that he learns new routes every time he visits a new city. When he asked me about my whereabouts, I introduced myself as a Mumbaikar and a financial advisor.

He couldn’t wait for me to complete… and started discussing his equity and mutual fund portfolio. This wasn’t new for me, as I had many such experiences in the past. In India, whenever we see a doctor or financial advisor, we start with our illnesses or portfolio discussions.

Two years back,

my Mom, out of a blue, started gardening.

She started with

3 plants (pots), which she bought from the market and placed it in the balcony.

Watering the plants, checking the soil and keeping a check on the plant’s growth,

become her daily obsession & favourite routine.

There’s very common saying “Do not keep all your eggs in same basket. Diversification means same, do not invest in only one asset class/only one sector. In India people generally prefer in investing in only two asset classes which are Gold & Real Estate.Historically they are known to give good returns & less risky,But in order to secure your portfolio from all ends & to earn more than inflation rate “Diversification” is very important.

Once you have selected the financial advisor/planner of your choice, the next step will be to meet them and discuss about your financial plan. Your advisor will need to ask you questions related to personal and professional matters to get to know you better and to device suitable plan for you. This means that you should be honest with your advisor with questions relating to these matters, especially when it comes to disclosing your income.

The purpose

of financial planning is to achieve your goals. Your goals help you to shape

your investments as per your requirement. Therefore, you must be very clear

about your goals before you start planning your finances. Your financial

advisor will also be able to help you better if you are clear with your goal. Here’s

what you should consider before finalising financial goals.

Portfolio Management Service (PMS) is a financial service

designed for High Networth Individuals (HNI). HNI investors generally prefer

customized investment options and thus PMS is suitable for such investors. PMS is

offered by various entities such as asset management companies, banks and

brokerages registered with SEBI. PMS Managers are highly qualified investment

professionals with extensive knowledge and research experience.

When it comes to planning you finances it will be best if you

seek help of a financial advisor. Not everyone has knowledge about financial

matters and it will be better if you take professional advice for managing your

finances. By managing your own finances or taking advice from friends and

relatives, you may not be able to successfully manage your finances and thereby

miss your goals.