It is important to consider the taxation rules before investing

Most people look only at the returns that an investment vehicle gives. It is, however, important to consider the taxation rules as well since this will reduce the overall returns. Here’s a look at some of these.

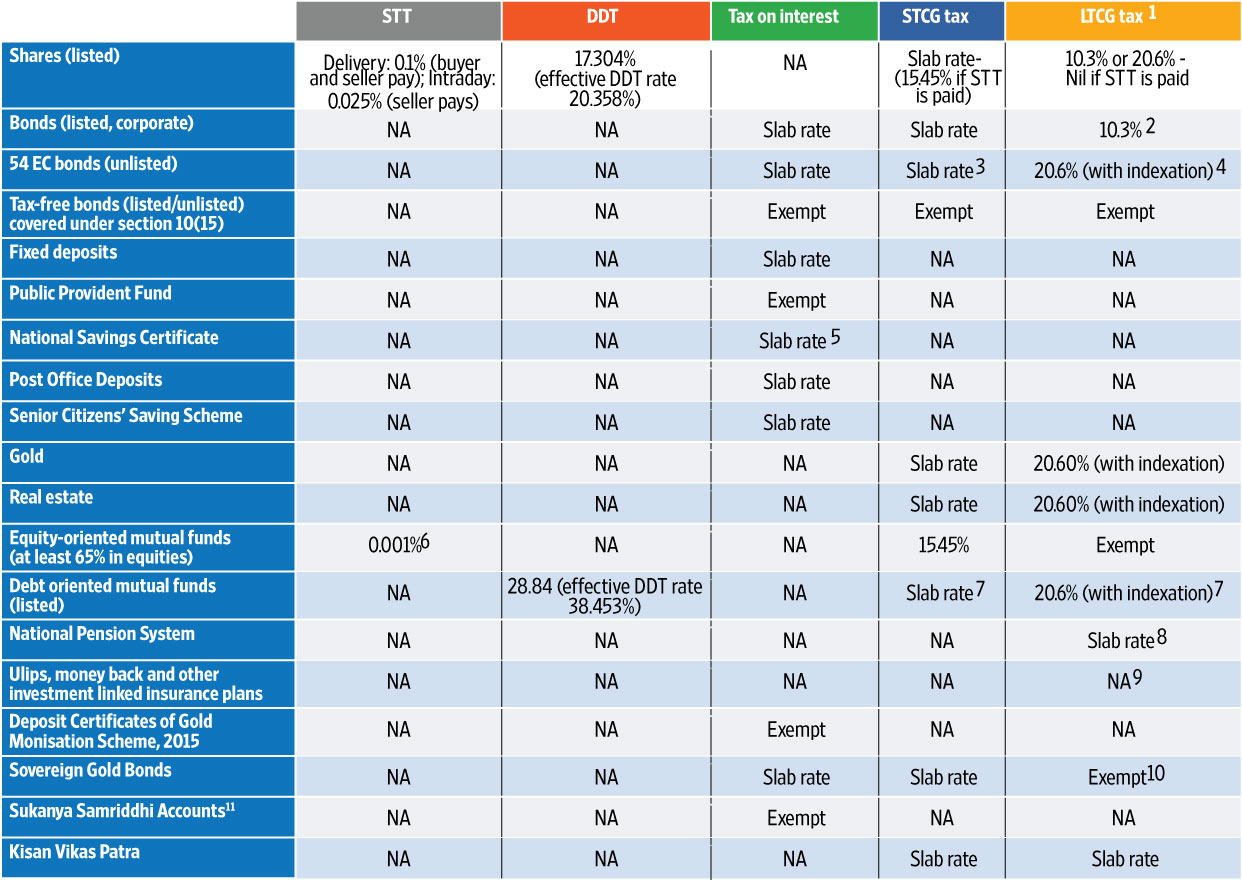

STT: Securities transaction tax; DDT: Dividend distribution tax; STCG: Short-term capital gains; LTCG: Long-term capital gains;

STT: Securities transaction tax; DDT: Dividend distribution tax; STCG: Short-term capital gains; LTCG: Long-term capital gains;

Ulips: Unitlinked insurance plans Tax rates given here are not inclusive of surcharge.

If the total income of nonindividual exceeds Rs1 crore, surchage @ 10% would be applicable.

The slab rates applicable would need to be increased by education cess of 3%

1LTCG tax rate is 10.3% without indexation benefits and 20.6% with indexation benefits;

2Bonds qualify as securities under the Securities Contracts (Regulation) Act, 1956;

3If 54EC bonds are transferred within 3 years of acquisition, then capital gains that was originally exempt will be taxed for LTCG;

4If 54EC bonds qualify as capital indexed bonds issued by the Government of India then LTCG will be taxed at 20.6% (with indexation);

5In the National Savings Certificate, the amount of interest allowed for tax deduction under section 80C is Rs 150,000;

6Payable by the seller at redemption or switch when selling to mutual fund;

7Post-Finance (No.2) Bill, 2014, the units of debt oriented funds, would be considered as a long-term capital asset if held for more than 3 years. Prior to this Finance Bill, these units were considered as long-term if held for more than 1 year;

8Withdrawals from National Pension System on maturity are tax free up to 40% of total corpus accumulated.;

9Any sum received under a life insurance policy (including bonus) is tax exempt provided premium for any year during policy term does not exceed 10% of sum assured;

10Transfer of Sovereign Gold Bonds under the Sovereign Gold Bond Scheme, 2015, by way of redemption, is tax exempt. If transfer is made before redemption, LTCG is taxed at 20.6% with indexation and 10.3% (without indexation) in case of listed bonds;

11A guardian can open only one account in the name of one girl child and maximum two accounts in the name of two different girl children.

Source: Mint research